The CPA Firms Moving First on Autonomous AI Will Be Hard to Catch

Written by Andrew Ross

The accounting profession has moved beyond asking whether artificial intelligence matters. The more urgent question is whether firms are moving fast enough, and intelligently enough, to avoid being left behind by a widening performance gap. CPA.com’s 2025 AI in Accounting Report describes AI as having shifted from experimental use to “essential infrastructure” and a “strategic imperative.” Thomson Reuters reaches a similar conclusion, identifying a growing divide between organizations with visible AI strategies and those without.

Moving cautiously is not a weakness in the CPA profession. It is part of its value proposition. CPAs are trained to be risk-averse because their work depends on accuracy, evidence, confidentiality, independence, and sound professional judgment. The hesitation around AI is often a response to legitimate concerns: hallucinated outputs, incomplete audit trails, data leakage, inconsistent results, and uncertainty over where professional responsibility ultimately sits. Any serious conversation about AI in accounting has to start with governance.

The Pace of Autonomous AI Adoption

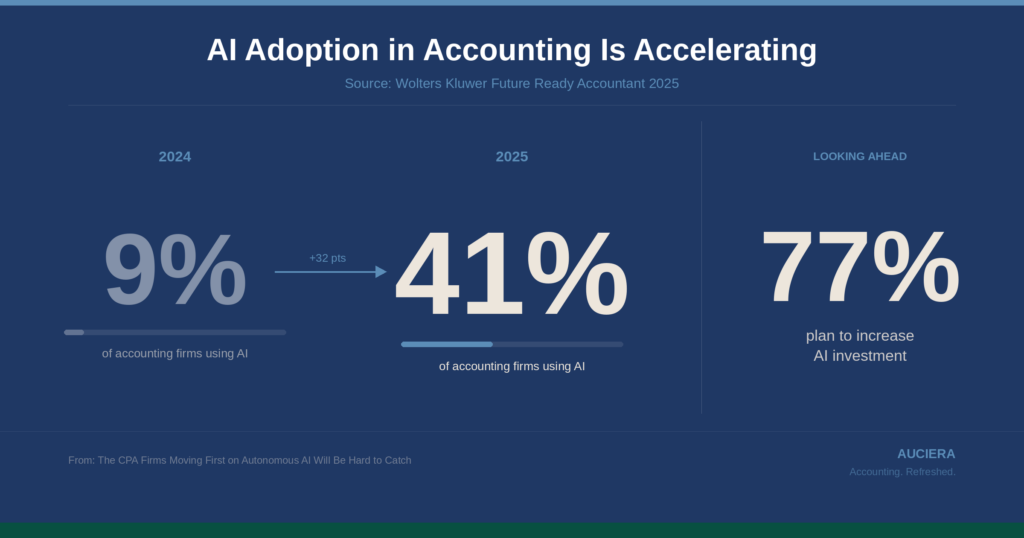

What makes the current moment different is the pace. Wolters Kluwer reports that AI adoption among tax and accounting firms rose from 9% in 2024 to 41% in 2025, with 77% planning to increase AI investment and 35% already using AI daily. Advisory services now reach 93% of firms, and AI use is increasingly tied to client service, workflow automation, and strategic insight generation. This is no longer fringe experimentation. It is the beginning of a new operating model for the profession.

| AI adoption among tax and accounting firms rose from 9% in 2024 to 41% in 2025. 77% plan to increase AI investment. This is no longer fringe experimentation. |

The more useful distinction is not simply between traditional software and autonomous AI. It is the distinction between AI tools and AI solutions. Tools help with narrow tasks: drafting emails, summarizing documents, answering questions. Solutions are embedded into the firm’s actual delivery model. They connect to workflows, data structures, review layers, policies, and client-service processes. In accounting, that difference matters. A firm may experiment with AI tools for months without changing its economics or service quality. Firms that implement AI as part of an end-to-end solution begin to change how work is performed, reviewed, priced, and scaled.

CPA.com’s 2025 research indicates that bookkeeping and automation are already AI-driven and moving toward fuller automation with agentic AI; tax preparation is approaching near-total automation in preparation, with significant AI augmentation in review; and workflow efficiency tools are expected to become ubiquitous across firms. Wolters Kluwer similarly described agentic AI at AICPA Engage 2025 as a shift from traditional automation toward intelligent agents capable of supporting or orchestrating audit and tax workflows.

That matters because early adoption appears to produce compounding returns. Thomson Reuters found that organizations with visible AI strategies were twice as likely to experience revenue growth from AI adoption as those using ad hoc approaches. The same report identifies a widening competitive gap and argues that firms that reinvent and automate entire business processes with AI will outperform slower movers through lower costs and better client experiences. Once a firm redesigns its workflows, review processes, pricing logic, and client delivery around AI-enabled solutions, competitors are no longer just catching up on software. They are trying to catch up on a different operating model.

The Productivity Advantage

The strongest immediate advantage is productivity, but productivity is only the first-order effect. Deloitte found that 42.7% of finance and accounting professionals identified greater efficiency and productivity as the leading benefit of AI agents. CPA.com goes further, arguing that as compliance work is automated, AI-powered insights create growth opportunities in advisory.

That shift has pricing implications. Thomson Reuters’ 2025 pricing research found that subscription and bundled pricing models are associated with greater pricing confidence and more successful price increases. CPA.com noted that AI-enabled tax workflows are helping move firms away from hourly billing and toward outcome-based pricing.

| AI can change not only how firms deliver work, but how they package and monetize value. The shift from hourly billing to outcome-based pricing is already underway. |

The Staffing Advantage

The staffing advantage may prove just as important as productivity gains. The profession is operating under persistent staffing pressure, and firms that use AI well can make work more scalable and more attractive. Wolters Kluwer reports that 31% of firms now cite advanced technical skill development as a top staffing challenge. CPA.com’s research indicates that new competencies will need to be developed, roles will continue to evolve, and AI-powered firms will have a significant competitive advantage in attracting and retaining talent. Firms that help professionals work at the top of their credentials, reduce low-value repetitive work, and build modern AI skills will have a clear recruiting and retention edge over those that preserve legacy workflows.

Autonomous AI with Strong Governance

A professional CPA audience should be skeptical of any claim that speed alone guarantees success. The evidence does not support that. Deloitte found that only 13.5% of organizations were already using agentic AI in finance and accounting, even though more than 80% of respondents believed AI tools could become standard within five years. The leading barriers were trust, integration into existing systems, and lack of skilled personnel. Most respondents said AI agents should operate only within a defined framework, with judgment calls remaining with people.

| In accounting, the winning model is not autonomous AI without humans. It is autonomous AI with controls, accountability, and professional judgment. |

The central risks are not abstract. They include unreliable outputs, weak source traceability, overreliance by junior staff, privacy exposure in client information, inconsistent application across engagements, and the possibility that a useful-looking output may still fall short of professional standards. That is why many firms remain more comfortable with AI as an assistant than as part of core execution. But that distinction will not hold forever. The firms that lead will be the ones that turn justified caution into disciplined implementation rather than prolonged delay.

From Tools to Solutions

The practical implementation challenge is not choosing an AI tool. It is building an AI solution on top of clean data, governed workflows, clear accountability, and effective integration. Deloitte has warned that AI-generated outputs in finance and accounting must meet expectations for accuracy, reliability, and trustworthiness, with effective controls including human oversight, data quality controls, audit trails, testing, and ongoing monitoring. NIST’s Generative AI Profile recommends inventorying third-party entities with access to organizational content, strengthening vendor due diligence around intellectual property, privacy, and security, and establishing contingency processes for failures in third-party AI systems. In plain English: bad data, fragmented systems, and weak controls will erase a large share of the upside.

This is why the profession needs to move beyond AI tools to AI solutions. A stand-alone AI assistant may improve personal productivity, but it rarely resolves the deeper constraints facing firms: fragmented workflows, limited leverage, inconsistent review processes, staffing bottlenecks, and pressure on realization. Solutions are different. They use AI inside a governed system of record and process, allowing firms to improve throughput, consistency, documentation, and client responsiveness without abandoning control. That is where the real strategic value sits.

Conclusion

The professional conclusion is straightforward: caution is rational, but it has a cost. The firms building lasting advantage are not experimenting with AI tools. They are implementing AI solutions that are trustworthy, integrated, and aligned with professional standards. That distinction is what separates a productivity experiment from a structural shift in how accounting work is delivered.

| Caution is rational, but it has a cost. The firms building lasting advantage are implementing AI solutions that are trustworthy, integrated, and aligned with professional standards. |

For CPA leaders asking what responsible, governed AI adoption looks like in practice, solutions designed specifically for the accounting profession are beginning to emerge. Auciera is one of them. Start a conversation.

This Editorial Opinion reflects the perspective of the Auciera team based on ongoing conversations with accounting professionals and regulators.

Author

Andrew A. Ross, CPA, CMA

Andrew Ross, CPA, CMA, is the Co-Founder and CEO of Auciera, an AI-native accounting platform built for accounting professionals and businesses that demand clarity, control, and confidence in their financial operations. Andrew brings over 25 years of accounting, tax, and financial management experience across public practice, consulting, and academia. He spent nearly a decade at two of the world’s leading professional services firms, serving as Senior Manager of Tax at EY and Performance Management Consultant at PwC, where he advised organizations on tax performance and enterprise financial decision-making. He has also held senior roles at Longview Solutions and MicroStrategy, giving him a deep understanding of how technology intersects with financial operations at scale. Since 2018, Andrew has served as a Professor of Accounting and Tax at Humber College, where he continues to shape the next generation of accounting professionals. His academic work reflects the same principle driving Auciera: that rigorous professional judgment and governance are non-negotiable, regardless of what tools are doing the work.

References

- Thomson Reuters, Future of Professionals Report 2025: Strategic AI Adoption: Unlocking Innovation and Maximizing Returns.

- Wolters Kluwer, 2025 Future Ready Accountant report.

- CPA.com, 2025 AI in Accounting Report.

- CPA.com, 2025 State of AI in Accounting Research Report and Shaping the future: 6 Takeaways from the AICPA and CPA.com AI Symposium.

- Deloitte, Trust Emerges as Main Barrier to Agentic AI Adoption in Finance and Accounting and AI transparency and reliability in finance and accounting.

- PCAOB, Staff Shares Observations From Outreach on Use of Generative Artificial Intelligence in Audits and Financial Reporting.

- NIST, Artificial Intelligence Risk Management Framework: Generative AI Profile (NIST AI 600-1).

- Accounting Today, How accounting firms use technology in 2025.